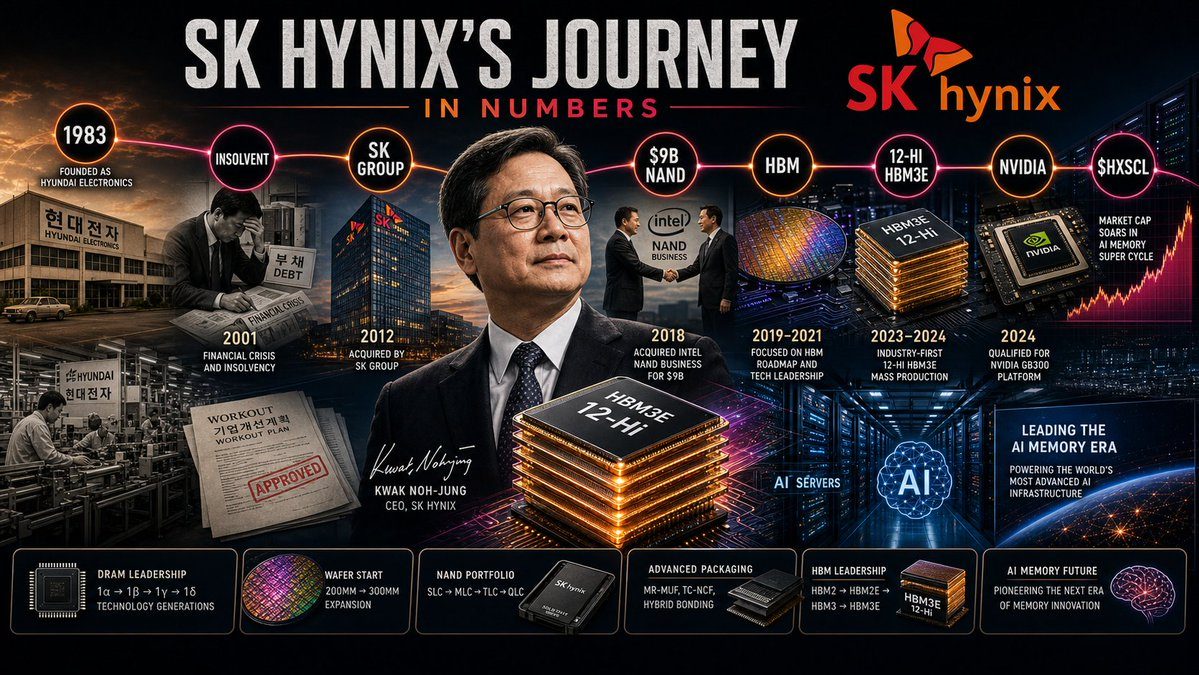

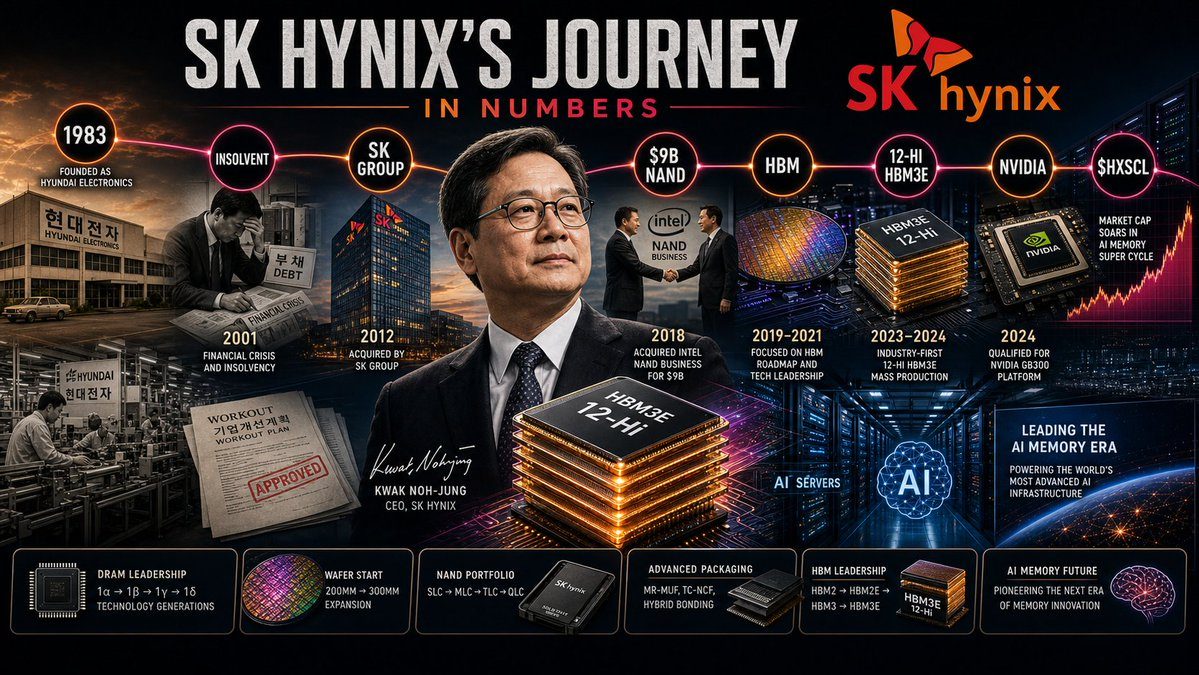

SK Hynix’s story is one of the great corporate survivals: technically insolvent and run by creditors in 2001, it reached the trillion-dollar club by 2026. Memory was always a brutal cycle business, and SK Hynix turned the latest cycle, AI, into something closer to a structural rent. Here is the journey, year by year.

- Founded in 1983 as Hyundai Electronics; spun off and left technically insolvent after the 1997–98 Asian financial crisis and the 2001 DRAM price crash.

- SK Group acquired it in 2012, providing the cash, scale and patience the previous owners lacked.

- A 2021 all-in bet on HBM, dismissed by many as niche, made it the sole 12-Hi HBM3E supplier to NVIDIA for 18 months.

- By 2026 it holds over 50% of the HBM market; Q1 2026 revenue hit ₩52.6 trillion at a 72% operating margin, and its market cap crossed $1 trillion.

1983 Founded as Hyundai Electronics Industries to build a memory-chip business for South Korea inside the Hyundai chaebol.

1996 Lists on the Korea Stock Exchange (now the Korea Exchange).

2001 The fallout from the 1997–98 Asian financial crisis and a brutal DRAM price crash expose the chaebol’s balance sheet; Hyundai Electronics is renamed Hynix Semiconductor, left technically insolvent, and creditors take it over.

2002 It sells stakes to anyone willing to buy in and goes through one of the largest corporate restructurings in Korean history.

2005 It emerges from creditor management, and survives.

2012 SK Group acquires the company, renaming it SK Hynix and bringing the cash, scale and patience the previous owners could not.

2017 SK Group acquires LG Siltron (renamed SK Siltron), securing the group’s silicon-wafer supply.

2020 It buys Intel’s NAND flash business for $9 billion, becoming the world’s number-two NAND maker overnight.

2021 SK Hynix bets the company on HBM; most of the industry calls it a niche, while SK Hynix calls it the only memory that matters for AI.

2023 It develops the world’s first 12-Hi HBM3 and ships samples to customers, with volume supply following in H2.

2024–2025 It is the sole supplier of 12-Hi HBM3E to NVIDIA’s GB300 for 18 months, as Samsung fails to qualify.

Q1 2026 A record quarter: revenue of ₩52.6 trillion (around $35.5 billion) at a 72% operating margin, both all-time highs.

May 2026 Market capitalisation crosses $1 trillion, only the second Korean company ever, with the stock up roughly 800% over the prior twelve months. CEO Kwak Noh-jung: “HBM4 demand from customers over the next three years exceeds our production capacity.”

2026 HBM market share above 50% makes SK Hynix the lead supplier of memory for the AI cycle.

The pattern is the point

From insolvent in 2001 to the trillion-dollar club in 2026, SK Hynix shows what the hardest businesses can do in the hands of the most patient owners. Memory was always a cycle; the HBM bet turned the AI cycle into a structural advantage. The deepest lesson is ownership: SK Group bought a near-dead asset and held it long enough for one well-timed wager to compound into the longest trade of the cycle.